There are many types of mutual funds, one of which is Liquid Funds. Most of the fund houses also provide facility to their investors to invest in Liquid Funds. Liquid Fund Investment is considered a better option for short-term investment.

If you are also looking to invest your extra cash somewhere and are thinking about liquid fund, then you are on the right article. Today we will know what are Liquid Funds and what are the differences between Liquid Funds and Fixed Deposits?

What is Liquid Funds?

Liquid Funds are a form of Debt Funds. Investments in Liquid Funds are not done in equity or stock market but they are invested in bonds. These bonds are short term with maturity of less than 91 days.

The returns of Liquid Funds are decided on the basis of the returns of these bonds.

Liquid Funds Meaning

As the name of Liquid Fund suggests, the amount of liquidity in these types of funds is very high. You can invest in it anytime and withdraw your money anytime.

Liquid funds are considered a good alternative to savings accounts and bank fixed deposits.

What do Liquid Funds invest in?

Liquid funds invest in safe instruments. These funds invest their money in bonds, government securities, debentures and treasury bills. These types of bonds have a predetermined interest rate.

The maturity of these bonds is up to 91 days only. Thus these bonds mature within 91 days.

Liquid Funds Returns

The returns of these funds range between 6 to 8%. Liquid fund return completely depends on the interest rate of the bonds. If the interest rate of the bonds is high then the liquid fund returns are also high.

Due to the slowdown in the economy due to the Corona virus lock-down, the interest rate of bonds also saw a fall. During this period, the returns of liquid funds remained around 4 to 5%.

Also read: Looking for investment? Here are Best Investment Plans With High Returns 2021

How much risk is there in Liquid Funds

Liquid funds are not considered risk free at all. There is definitely a risk in them but its quantity is very less. As Liquid Funds invest in debt instruments, there is always the risk of interest rate fluctuations. For this reason, the NAV (Net Asset Value) of liquid funds also fluctuates.

The second risk in these funds is credit risk. There may be times when the money of the bonds may not come back. If we understand in simple language, to whom the fund house has given his money, he cannot return the money back.

This is mostly seen in corporate bonds. Govt. Bonds are considered almost safe. Despite all this, the risks in liquid fund investments are manageable due to the fund manager’s portfolio diversification.

Exit Load in Liquid Funds

There is no entry load in Liquid Funds but there is definitely an Exit Load. According to the new guidelines of SEBI, if you do not sell your investment in Liquid Funds for 7 days, then you will not have to pay any Exit Load.

But on selling your investment within 7 days, you have to pay a small Exit Load.

How do Liquid Funds work?

Whenever you deposit money in any liquid fund, the fund manager of that fund invests your money in bonds, government securities. It is a regular process which goes on continuously.

The NAV of the liquid fund is worked out on the basis of the interest rate of these bonds. The NAV is calculated on every working day. Due to the fixed returns of bonds, the value of liquid funds does not fluctuate much.

Expense Ratio in Liquid Funds

The expense ratio in liquid funds is slightly lower as compared to equity funds. SEBI has fixed the maximum limit of expense ratio on Liquid Funds at 2.25%.

Examples of Expense Ratios of Some Popular Liquid Funds –

ICICI Prudential Money Market Fund – Direct Plan – 0.21%

Kotak Money Market Fund – Direct Plan – 0.22%

Quant Liquid – Direct Plan – 0.62%

Liquid Funds Tax Treatment

Dividends in Liquid Funds are taxable as per the normal tax slab. Liquid funds are taxable in two ways.

STCG- When liquid funds are sold for 3 years or earlier, STCG tax is applied on it. In case of STCG, profits are added to the annual income of the investor. In this, tax is imposed as per the tax slab of the investor.

LTCG- If the liquid fund is sold after three years, then LTCG tax is applicable on that profit. Currently LTCG rates are 20%. LTCG only seems to impose on profits exceeding one lakh rupees.

Let Mahesh have a long term capital gain of Rs 1,50,000. In this case, Mahesh will have to pay capital gains tax only on ( Rs 1,50,000 – Rs 1,00,000 = Rs 50,000 ). Here total LTCG = Rs 50,000 × 20% / 100 = Rs 10,000.

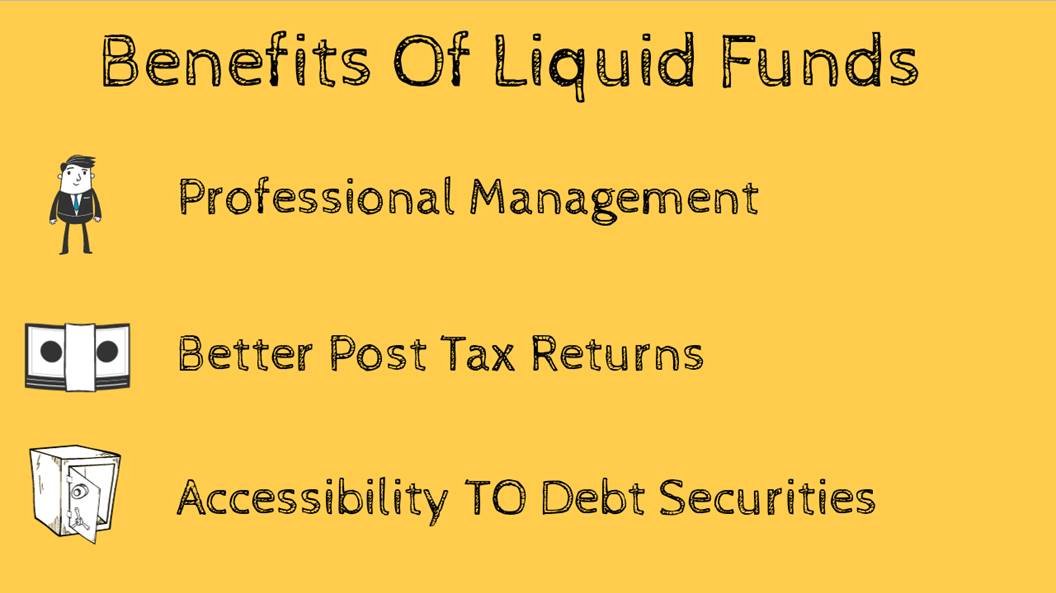

Benefits of investing in liquid funds

1. Good Returns- In recent times, the returns of liquid funds are better than savings accounts and most fixed deposits. Liquid funds can be the best return option for personal investment in times of high inflation.

2. Low Risk- Investing in short term bonds of Liquid Funds protects the investor from the risk of changes in interest rates. Thus, they carry very little risk.

3. Liquidity- Money can be easily put into a liquid fund and can be withdrawn anytime when required. There is no lock-in-period in this.

4. No Exit Load- If you remain an investor in a liquid fund for 7 days and redeem your money after that, then you do not have to pay any exit load. In this, only after withdrawing the money within 7 days, a nominal Exit Load has to be paid.

5. Diversification- If you invest in equity funds, then you can also invest a little in liquid funds, so that your investments remain diversified.

Saving Account vs Liquid Funds

In recent times, almost all the big banks have reduced their savings account interest rate significantly. The rate of interest on savings account is around 3.5 to 4%.

If the inflation rate is considered to be 5%, then the value of your money will decrease between one to one and a half percent annually, even if it is in the savings account. If we talk about liquid funds, then they give more returns than savings accounts and also help you to deal with inflation.

In conclusion, it can be said that liquid funds are a much better option than a savings account. You can invest some of your extra cash in liquid funds.

Also read: 10 tips on money and finances to follow before 30

Fixed Deposit vs Liquid Funds

There is always a question in the mind of many investors that where to hold the extra cash? If you have the option of fixed deposits and liquid funds, which option would you go with? You will get the answer of this fixed deposit vs liquid funds from the differences mentioned below.

Difference between fixed deposit and liquid fund

1. Risk

Fixed Deposit- FDs are mainly offered by banks or NBFCs. Therefore, there is almost negligible risk in it.

Liquid Fund- The main investment of liquid funds is in fixed income instruments. The interest rate of these bonds depends on the volatility of the market and the economy. So there must be some risk in them.

Winner- Fixed Deposit

2. Returns

Fixed Deposit- FD has a fixed rate of interest. It comes under the purview of RBI regulation. Currently, almost all FDs have interest rates of less than 6%. The rate of interest on FD depends on the financial system and economy of the country. FD returns are higher than savings accounts but lower than liquid funds.

Liquid Fund- Unlike FDs, Liquid Funds do not offer any guaranteed returns but still their returns are higher than FDs.

Winner- Liquid Fund

3. Liquidity

Fixed Deposit- You cannot redeem FD prematurely. If you prematurely cash out the FD, you have to pay some penalty. This penalty is usually 1% of the returns.

Liquid Fund- After the seventh day of investment, you can redeem the liquid fund whenever you want. Exit load has to be paid if redeemed before 7 days.

Winner- Liquid Fund

4. Taxation

Fixed Deposit- The return or interest of the fixed deposit is added to the income of the investor. Returns are taxable as per the tax slab of the investor. If the interest income is more than Rs 40,000, then the bank deducts 10% TDS on the maturity of the fixed deposit and gives it to the investor.

Liquid Fund- If the liquid fund is sold for more than 3 years, then LTCG tax is imposed at 20%. Returns are taxable by adding to annual income if sold for less than 3 years.

Winner- No clear winner

5. Top-up Facility

Fixed Deposit- Apart from Recurring Deposit, no additional investment facility is available in normal FD. If you want to make a new investment, then you will have to get a new FD.

Liquid Fund- You can make additional investments in liquid funds whenever you want.

Winner- Liquid Fund

6. Tax Benefits

Fixed Deposit- If you invest in FDs with a lock-in-period of 3 or 5 years, then you get exemption under Section 80(C) of Income Tax.

Liquid Funds- There are no tax benefits available in liquid funds.

Winner- Fixed Deposit

Conclusion

In our opinion, if you want to invest your extra money somewhere without any risk then you can invest in fixed deposit.

If you want to get high returns by taking a small risk, then liquid funds can be the best option for you. Both these options come with their own advantages and disadvantages. You can choose any one as per your need.

FAQ

1. Are Liquid Funds Risk Free?

Liquid funds have very low risk. It is based on the interest rates and credit risk of the bonds.

2. Can I withdraw money from Liquid Funds whenever I want?

Yes, you can withdraw money from Liquid Fund whenever you want.

3. Can SIP be done in liquid funds?

You can invest in both Lumpsum and SIP types in Liquid Funds.

4. Can liquid funds give negative returns?

Liquid funds can give negative returns in a very short period of time. But it is almost impossible to have negative returns in liquid funds in casual long run.

Also read: Best Stocks To Buy India For Short Term (2-3 Years)

5. Are Liquid Funds and Debt Funds the same?

Debt funds are a type of mutual fund. The same liquid funds are a type of debt funds. The risk in debt funds is slightly higher than in liquid funds.